I have recently been a part of a few M&A processes at companies I work closely with. These transactions involved private companies selling to larger companies (public and private) and were all-cash transactions.

This inspired me to chronicle best practices and considerations for founders who are selling their company. In doing so, I hope that founders take away at least one useful insight.

I am grateful and fortunate that I could solicit input on this article from several people, including Theresia Gouw and Mark Kraynak; a few of my partners at Acrew; Ed Zimmerman and Meredith Beuchaw from the law firm Lowenstein; Shan Aggarwal, VP of corporate development, Coinbase; and Art Levy, chief strategy officer at Brex. I hope to also hear from more founders as they read through this.

First, some observations

M&A can be a great outcome for all parties, especially for startup founders and their team. Founders may have conflicting emotions when thinking about selling their company. That is perfectly understandable; in the beginning, many founders hope to build an enduring company.

Not all companies are best positioned to go it alone, and that’s okay.

However, it’s important to acknowledge that there are plenty of good reasons to sell: You can join a “larger rocketship” where 1+1=3; there could be a strong match with an acquirer; burn-out in the startup team; the team or investor wants liquidity; and so on. Further, myriad long-term, standalone companies have been founded by founders who sold or exited their prior companies.

During downturns, think of M&A as a game of musical chairs. The companies that test the market earlier in the cycle (before things have gotten particularly bleak) tend to see better outcomes.

In markets where incumbents are playing catch-up, there is a window when a few companies will get bought. By the time those deals settle, the rest will likely decide to build instead of buying.

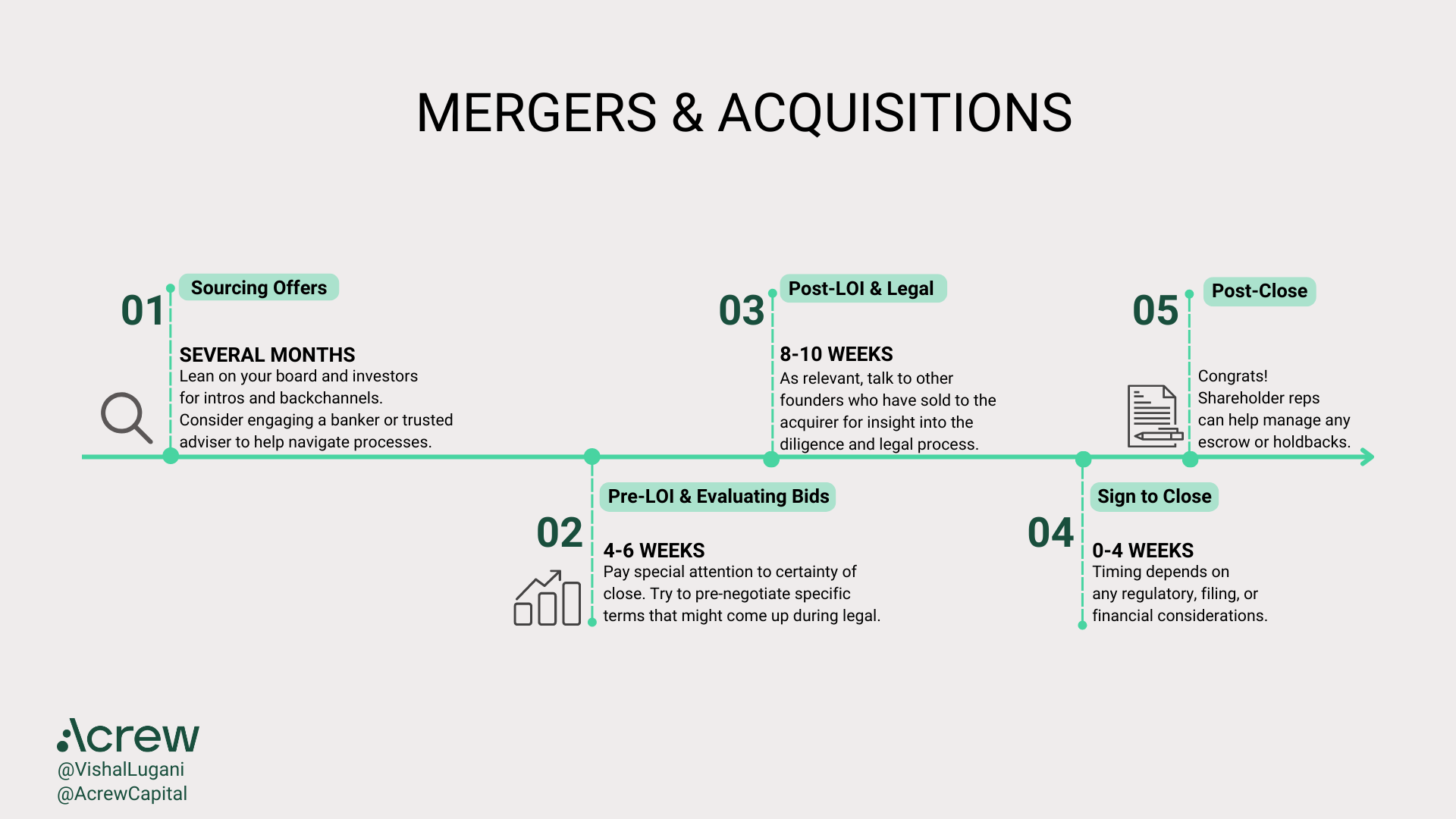

Below, I’ve outlined the key steps of a M&A process.

From a timing point of view, founders should plan to conclude a sale in up to nine months. That isn’t to say it can’t happen sooner, but we would counsel that amount of cash buffer. This may require companies to raise bridge financing and/or consider reducing burn. As one of my partners counseled, “Every week you wait to cut spend makes the cuts you will need hurt that much more.”

Image Credits: Acrew Capital

Sourcing offers

- This entails months of building relationships. Before a process, finding offers could take anywhere from several weeks to a few months to get all parties engaged and working.

- You’ll want to share any offers with your board and key investors to make sure you’re atop all governance requirements.

- It’ll be useful to build relationships with bankers as well, because they are in the market and talking to acquirers frequently. This will help you stay top of mind in your industry and be included for everything from conference invites to market maps.

Pre-LOI and evaluating bids

- Again, this can take several months. A highly motivated acquirer running a tight process should be able to get through diligence in two to four weeks, but that would be fast in any market. You need to account for competing priorities at the acquirer, any other deals that might come up for their corporate development and personnel schedules.

- Your leverage declines after you sign a LOI. In many cases, the LOI puts you into a period of exclusivity with the buyer. That’s why it’s important to nail down the details on the terms right away.

- Consider getting representation and warranty insurance (RWI). This will influence how much of the deal consideration is paid upfront and how much is “at risk,” where selling shareholders will be at risk of losing proceeds earmarked or distributed to them.

Post-LOI confirmatory and legal diligence

- Generally, diligence at this point should be less strategic and more operational. Legal diligence, however, will be exhaustive, and you may find that more detailed terms are being either negotiated or renegotiated via definitive long-form deal documents. It’s important to plan for this process with your legal counsel.

- If you opted for an RWI, the insurer will also run diligence on the company.

A timeline for startup M&A processes: Key steps and factors to consider by Ram Iyer originally published on TechCrunch

DUOS